—

Airbnb finally went public and its share is traded above $100. Now, the question should be asked, what is the fair value for the stock? To answer that question, we need to analyze the company´s financials as well as future perspectives that will play a crucial role in the results and overall performance.

ABNB stock chart by TradingView

In the context of the Covid-19 pandemic, many hotels had to close permanently or operate at a fraction of their available capacity. This could not but cause a sharp sell-off in equity markets across the globe. So-called beach industries – booking, entertainment, airlines, cruises, and hotels – were hardest hit by the lockdowns and quarantine measures.

Airbnb was no exception. According to its S-1 filling (the initial registration form for new securities required by the SEC for public companies that are based in the U.S.), during the nine months ended September 30, 2020, our business was materially impacted by the global COVID-19 pandemic, with GBV of $18.0 billion, down 39% year over year and revenue of $2.5 billion, down 32% year over year. Its Free Cash Flow fell $839.9 million to $(520.1) million on a year over year basis. Net loss was of $696.9 million, representing a decrease of $374.1 million year over year; and Adjusted EBITDA went to $(230.2) million, a decrease of $253.3 million year over year.

Even though, the company insisted that within two months, its “business model started to rebound even with limited international travel, demonstrating its resilience. People wanted to get out of their homes and yearned to travel, but they did not want to go far or to be in crowded hotel lobbies. Domestic travel quickly rebounded on Airbnb around the world as millions of guests took trips closer to home. Stays of longer than a few days started increasing as work-from-home became work-from-any-home on Airbnb.“

If we consider that many investors/traders are following the greater fool theory (which states that it is possible to make money by buying securities, whether or not they are overvalued, by selling them for a profit at a later date), we could say that valuation doesn’t play any role. In other words, they believe that there will always be someone (i.e. a bigger or greater fool) who is willing to pay a higher price.

This strategy is very risky ends up creating actual bubbles that eventually burst. And the reason is the clear overvaluation of the company. The question should be then asked: how the value is determined? One of the ways is to estimate the company’s capacity to generate and grow (potential) cash flows. Additionally, demand and supply play an important role in the price of an asset. Thus, besides the corporate fundamentals or multiples, the share of a company is determined by market sentiments and liquidity (illiquidity).

Another important tool in analyzing the company´s valuation is to compare it with the nearest competitors or at least similar to the target company. To be more precise, we would need to compare their multiples. The only problem is that it isn’t easy to find a comparable firm. For example, in the case of Airbnb could we compare it with Marriott? The first company doesn’t actually possess any physical space itself, it’s an IT company, whereas Marriott owns over 4,000 physical properties.

The second step is to analyze where the company´s revenue comes from. On the one hand, Airbnb charges a 3% commission upon every booking from hosts and a 6-12% commission from lodgers. Thus, the biggest proportion of the profits come from recurring fees. The major costs, meanwhile come from Technological running & development costs, Salaries to employees, and Marketing and Management costs. In the context of Covid-19, the company was forced to reduce its fixed and variable costs including a reduction in force and a suspension of substantially all discretionary marketing program spend.

Looking at key business metrics to measure Airbnb´s performance, in 2020 its Nights and Experiences Booked declined 41% from 251.1 million to 146.9 million.

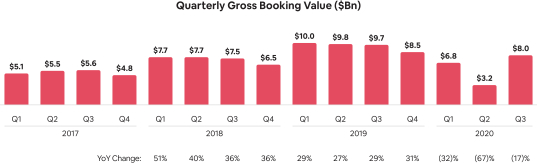

Gross Booking Value, which represents the dollar value of bookings on our platform in a period and is inclusive of host earnings, service fees, cleaning fees, and taxes, net of cancellations and alterations that occurred during that period, was $18.0 billion, a 39% decrease from $29.4 billion for the comparative prior-year period. On a constant currency basis, the reduction in GBV was 39%.

Finally, Adjusted EBITDA was $(230.2) million, compared to Adjusted EBITDA of $23.1 million in the prior-year period. The decrease was due to the reduction in Nights and Experiences Booked and GBV due to the COVID-19 pandemic, as described above, offset by cost reductions.

In terms of profitability, Airbnb incurred net losses of $70.0 million, $16.9 million, $674.3 million, and $696.9 million for the years ended December 31, 2017, 2018, and 2019 and the nine months ended September 30, 2020, respectively. Due to coronavirus, the company has got into additional costs, thus they may not succeed in increasing our revenue sufficiently to offset these higher expenses. In particular, they expect the ongoing economic impact from the COVID-19 pandemic to have a material adverse impact on our revenue and financial results for 2020 and beyond. Even though, it is important to mention that Airbnb is closer to profitability than companies like Lyft and Uber.

Overall, looking at the industry evolution, Airbnb could continue to grow, eventually reaching profitability. However, for that Airbnb will have to achieve growth in gross bookings. It is also worth mentioning that the company doesn’t have a ton of debt. Even though, its future also depends on the recovery from Covid 19 and vaccine evolution. It is crucial to follow the company´s operating margins evolution

At the moment, the share of Airbnb is clearly overvalued. First, the company targeted an IPO price of between $44 to $50 per share, then it has been raised to between $56 and $60 per share. Currently, it trades at $120+.

According to Aswath Damodaran analysis,

If equity is priced at <$28 billion (20% percentile): A bargainIf equity is priced between $28 & $33 (40th percentile) billion: A solid buyIf equity is priced between $33 (40th percentile) & $38 billion (60thpercentile): A fair valueIf equity is priced between $38 (60th percentile) & $44 billion (80thpercentile): Too richly pricedIf equity is priced > $44 billion: Over valued

Howbeit, always do your own research. Don’t get fooled by the hype and analyze possible risks.

—

This content is brought to you by Igor Kuchma.

Inset photos provided by TradingView.

Feature photo: Shutterstock